Introduction

Xero Video help:

https://www.xero.com/uk/features-and-tools/accounting-software/fixed-asset-management/

Online course:

https://central.xero.com/s/learning-search#q=fixed%20assets

One gets into the realm of fixed assets and their depreciation if you acquire or purchase an item the cost of which should be spread over more than the current year. It should then be shown as a fixed asset in the accounts and the cost shown as depreciation over the relevant period. (It follows that if all the cost can be allocated to the current year, then there is no point in treating the related item as an asset; instead allocate the cost to an appropriate expense code.)

So, for example, if we buy a computer for £1000 that is expected to last 4 years, we record it as an asset and have as an expense depreciation of the asset at £250 per annum. This implies that we need to retain in the accounts the original cost of those assets in order to apply 25% depreciation every year.

This is achieved by the pairing of an undepreciated value of assets by type (Office equipment, Computers, etc.) and the cumulative depreciation for assets of that type. In the case of Computer equipment these are accounting codes 720 (Computer equipment, original value) and 721 (Cumulative deprecation of computer equipment).

In general the way this works is that the initial purchase is coded to the original value asset code (e.g. 720). Then at year end depreciation is applied at 25% of the original value debiting the value to Depreciation and crediting it to the appropriate cumulative depreciation account.

(In relation to fully depreciated assets, accounting practice seems to be as follows: An asset that is fully depreciated and continues to be used in the business will be reported on the balance sheet at its cost along with its accumulated depreciation. There will be no depreciation expense recorded after the asset is fully depreciated. When the asset is disposed of through retirement, sale, salvage, etc., it is then removed from the balance sheet.)

If you have high value fixed assets where it would make a material difference to the accounts how accurately they were depreciated (e.g. it makes a big difference for how many months of the year depreciation applies), then you should maintain a fixed asset register and have Xero compute and apply depreciation and thus also maintain suitable book values for the assets.

This is something that requires Advisor permissions in Xero. It may therefore be something you want to leave to your accountant/auditor. It is not very complicated, though, and should not present too much difficulty by following the Xero help:

https://central.xero.com/s/article/Register-fixed-assets

https://central.xero.com/s/article/Run-or-roll-back-depreciation?userregion=true

If you only have a few, low value assets, then you could omit registering assets in Xero and keep your own records of purchases and related depreciation in a spreadsheet; then you could simply apply the total annual depreciation needed for each class of assets (Computer equipment, Buildings, Office equipment) via manual journal entries for each class, debiting the value to Depreciation and crediting it to the appropriate cumulative depreciation account. (Note that you would also need to reduce both the original value asset account and its paired cumulative deprecation account for each asset disposal.)

The advice here is to register assets in Xero in all cases. It is preferable to keep all the necessary information in Xero and it is no harder, probably easier in fact, to do this than to keep an external register and to pass data manually between the systems. The process below assumes asset registration in Xero.

Process

The processes described here do not cover importing historic assets and their depreciation into Xero when first moving over to Xero. For this see Xero help at:

https://central.xero.com/s/article/Import-fixed-assets-UK

https://central.xero.com/s/article/Enter-opening-balances-for-fixed-assets

Neither are Fixed Asset Settings described here. It is presumed that the Advisor who sets these needs no extra guidance.

Bills for fixed asset purchases

The best way of setting up registration of fixed assets is simply to code the line items in related bills to the Original value asset code for the relevant asset type, e.g. 720 Computer equipment. This not only adds the item value to that account; it also creates a Draft asset ready for registration by someone with the Advisor role.

If there is no bill for the purchase (which means that transaction account codes are applied in reconciling bank transactions), then again use the Original value asset code for the relevant asset type at that point.

Recoding bills or transaction for assets

Corrections of bills or spend money transactions will NOT have the effect of creating Draft assets for registration. So in these cases, you will need to let the relevant Advisor know about the correction so that they can add the asset to the Xero register manually.

[Note from Xero support:

“Whenever Expense Claims, Bills or Spend Money payment transactions are entered using an account code that has a Fixed Asset account type, a Draft asset is automatically created in Fixed Assets.

However, this only happens when these transactions are approved for the first time. If an approved bill or spend money transaction is edited and the account code is changed to one with a Fixed Asset account type, a draft asset won’t be created.”]

Bringing depreciation up to date

This has to be done by someone with the Advisor role. We assume here that settings for all relevant asset types have been done appropriately. There are then three things to do:

- Check that assets no longer in use have been disposed of in Xero; dispose of relevant assets where not.

- Register draft assets, checking in each case for appropriate Activity/Class and Donor/Project entries and potential errors, adding notes as appropriate.

- Run deprecation to the desired date.

Depreciation will then be calculated up to the desired date but no further. Additions or changes to assets relating to the period for which depreciation is computed will result in a recalculation of the depreciation (and hence also of the related cumulative depreciation accounts).

Taking an asset out of use

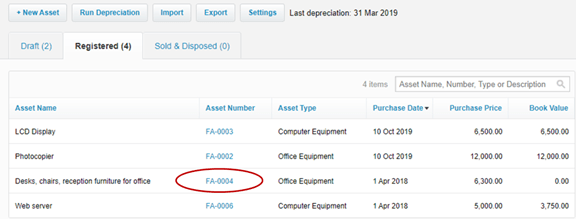

Whenever an asset in the register is taken out of use, then it should be removed from the accounts. Notify the Advisor who handles Fixed Assets of the change and the asset. They will identify the item in the asset register and get the option to dispose of the asset by clicking on the asset number.

The individual asset view has an Options drop down, where you click on “Dispose”.

This moves the asset to the Sold & Disposed Category and reduces the Original value and cumulative depreciation account values for the related asset type.

Recommended options for the disposal process:

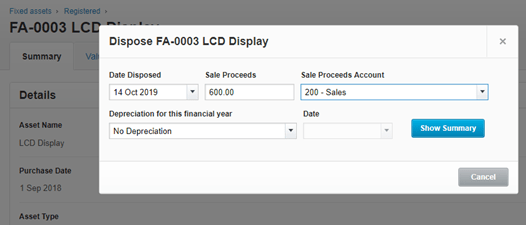

The first prompt box is as below. If the item is being scrapped, put “0” in the Sale Proceeds box; otherwise put the sale proceeds value and have the associated account be “200-Sales”. Select “No depreciation” for the depreciation option. Then press “Show Summary”.

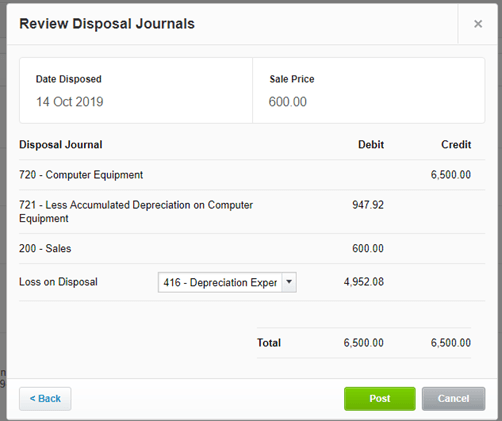

This will bring up the following expansion of the prompt box. (Only the first two lines will appear if the item is fully depreciated and being scrapped.) Press “Review Journals”.

In the final prompt box, select “416 – Depreciation expense” for any positive loss on disposal shown. Then press “Post”. In the more typical case of scrapping a fully depreciated asset, only the first two lines (with equal values and for the relevant asset type) will be shown.